During the first half of 2020, there has been a growing debate in the startup and SME ecosystem in Africa on the type of capital flowing into Africa and the actual beneficiaries of that capital. There have been several arguments and counter-arguments’ but from where I sit there are two key conclusions I have drawn from this debate. The first is the fact that there is an ever-growing need in Africa for early-stage funding in various forms for startups, micro, small and medium enterprises (MSMEs). The African Development Bank(AFDB) estimates that out of the nearly, 420 million youth aged 15 to 35, only one out of six are in wage employment. The five out of six who are not in wage employment will likely end up in entrepreneurship and will require funding. The second conclusion I draw is that the current funding supply structures comprising of legacy financial institutions and private funders cannot possibly meet this ever-growing demand for early-stage capital. This, therefore, means that there is a need for new funding structures to ensure more local or international capital is mobilised into African businesses.

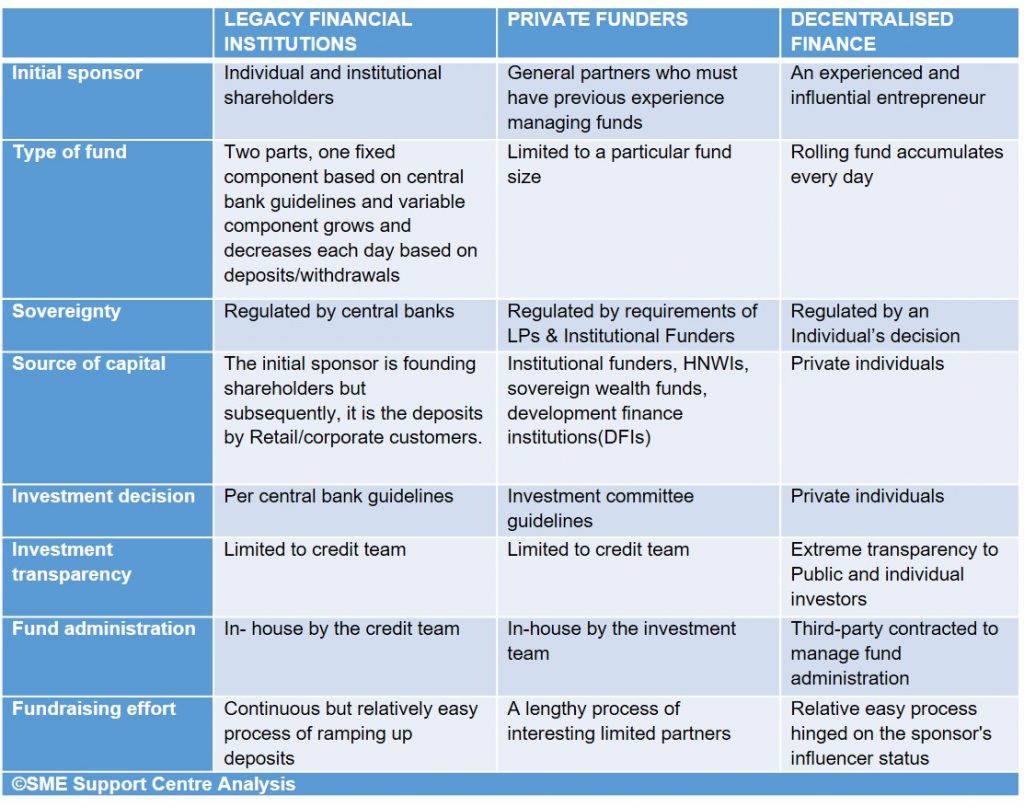

On April 10th,2020, Mr. Inoluwa Aboyeji a respected African entrepreneur and founder of Andela and Flutterwave announced the formation of the “Future Africa Fund” based on two key concepts “decentralized finance” and “rolling funds’’( https://angel.co/v/back/future-africa). Since then there have been several announcements’ by other similar experienced and influential entrepreneurs, most recently including, Mr. Sahil Lavingia, the founder of Gumroad. Am sure you are wondering, how these two concepts will change the funding landscape in Africa and beyond? To guide you, I have provided an illustrative below.

Decentralized finance as a concept allows an experienced and influential entrepreneur in a particular field, to壯陽藥 mobilize capital for early-stage investments on a rolling basis from the public or as many retail investors as possible. It also provides for an element of choice since each investor is provided with an array of carefully reviewed enterprises to choose from and they are free to decide in which enterprise they will put their money. The structures that the concept of decentralized finance provides could allow for a more structured way of increasing the supply of capital whether local or international to African businesses. We have so far only seen, the concept tested by successful entrepreneurs focused on high-growth tech startups, backed by fund administrative processes provided by Angel List. Now the question remains, how can the same be replicated to a majority of African micro, small and medium enterprises who are low/ medium- growth enterprises and not tech-based? What local administrative structures can we take advantage of in Africa to ensure, decentralized finance can ensure more and more local capital is mobilised for African businesses?

The commercial banks and micro-finance institutions (MFIs) in Africa have for a long time been the go-to financiers for any Micro, Small or Medium enterprises, as long as they have the collateral to back up their request. These legacy financial institutions have also been the largest beneficiaries of retail capital from the deposits of the millions of institutional and retail customers that they serve. This is a key premise of the concept of decentralized finance, mobilizing capital from a wide range of people. These institutions have the required administrative structures and technology to manage the lending and flow of capital into African businesses. The missing link is the element of free will and choice on which investment by the millions of retail depositors/investors. These institutions have had their investment decisions highly regulated by the central banks primarily because they do not lend their own money. Thus, can we re-imagine a future where this choice is decentralized? What would it take to re-imagine this future?

Re-imagining commercial banks and MFIs as decentralized would require policy changes and would perhaps open up an era of less regulation by the central banks. The deposits will continue and staff within the commercial banks would still source, review, and present possible loan applications or investment deals to any potential up taker/customer. The customers would be eligible to commit to any investment based on their level of deposits. The bank staff will also manage the disbursements and collections in exchange for stipulated fees or any revenue share arrangements. It can start as a pilot that offers customers the flexibility to sign up for such a scheme. I believe these radical thoughts would change the future of what banking looks like and would perhaps ensure that more local capital is mobilised to meet the ever-growing funding gap for micro, small and medium enterprises in Africa.